Student Loan Repayment. I hate student loans. If you are reading this article, my guess is that you are not too fond of student loans either. Most of us (yes, I said us) would like nothing more than to just tell our student loans to GTFO.

But sadly, most of us don’t. In fact, it takes the average undergraduate degree borrower 20 years to pay off their student loans. 20 years! And to make it even crazier, it takes the average professional degree holder 46 years to pay off their student loans! 46 years!

Think about it. If the average professional (a JD, MD, DVM, PharmD, etc.) finishes school at 30, they won’t have their student loans paid off until 76! You know what that means? A lot of them will never pay off their student loans. Some people will literally die before their student loans are paid off. And for most professional borrowers, they will spend nearly their entire career paying for the education that they had to get to have that career in the first place.

After all, there are about 42 million Americans with student loan debt right now. That is roughly 13% of the entire population. That. Is. Crazy.

While we’re at it, lets go over some student loan repayment stats that will make you want to cry a little bit.

- 55% of borrowers see their overall balance of student loans INCREASE over the first five years of repayment.

- The average student loan debt is $37,651.

- The student loan debt growth rate outpaces the rise in tuition costs by 353%.

- The total student loan indebtedness in the US is roughly $1.6 trillion.

- 53% of millennials are disqualified from purchasing a home because of their student loan balance.

Before I get to the actual meat and potatoes of this article (the different types of student loan repayment options), let me make a couple caveats.

- Let me first tell you something with as much gusto as I can muster. The only way that you are going to get rid of your student loans is if you pay them off. Let me say that again just in case you are skimming this article and not reading it fully. The only way that you are going to get rid of your student loans if you pay them off.

Yes, there is a chance that the federal government can actually follow through with their student loan repayment promises. But I don’t know about you, but I don’t put my life on hold or otherwise depend on the government to pay anything for me. If it happens, cool. I will be the first one to cash the check. But if you live your life dependent on anyone else (especially the federal government) to help you (and especially to pay off your debts), you are making a big mistake.

- Do not depend on the Public Service Loan Forgiveness Program. The Public Service Loan Forgiveness Program does not work. In fact, roughly 99% of applicants that have applied for it (after making payments for 10 years as instructed by the program) have been denied. And if the Public Service Loan Forgiveness program doesn’t work, why would you expect that the standard 20 or 25 year forgiveness program (that will be discussed later) would work? Why would you stake your financial future on a program that works only 1% of the time. No friggin way.

- Your attitude should be to get your student loans paid off. ASAP. My guess is that if you are reading this, you are more likely to want them to be paid off sooner rather than later. But if you aren’t one of those people, please don’t just make the payments for 20 years (remember that is the average for an undergraduate) like everything is normal.

- Do not think that the federal government will pay off your remaining balance in 20 or 30 years. That is just ridiculous. No one has any idea what financial condition the government will be in 20 or 30 years or if they decide to do away with that program. Also, the federal government can change the terms of a student loan contract at will. If you are thinking that you will just make the smallest payment possible until the government will pay off the rest, please don’t set yourself up for that. If they don’t follow through you will be royally screwed.

Man, I sound cynical.

Let me tell you what this article will NOT be about:

- Recommendations of what student loan repayment option to choose (suggestions will be given but you need to make the final decision based on your own circumstances).

- A recommendation of which, if any, student loan consolidation company to use.

- Bashing you over the head for taking out student loans. I will never make someone feel poorly because of their current financial situation. Just like I would never make fun of someone because of their weight. If you have student loans, that’s okay. Let me help give you the tools and knowledge to get them out of your life.

So here we go.

(1)

Standard Repayment Plan

Of all the student loan repayment plans, the Standard Repayment Plan is the simplest and most straightforward. With this plan you will pay the same amount over a fixed period of time (anywhere from 10-30 years). The repayment of this loan looks just like if you had a car payment (just a really big car payment). Here are some pros and cons of the standard repayment plan as well as a graph of what it looks like in the 10 year Standard Repayment Plan.

Pros:

- With this plan, you will pay the least amount over time.

- You can choose a plan to pay your student loans off in as little as 10 years.

- You don’t have to resubmit any paperwork while in repayment to verify income, employment, work status etc.

Cons:

- Your payments will be the most of any of the student loans repayment options.

Remember, you can (AND SHOULD) pay extra on your student loans to pay them off sooner. Your payment on your student loans (or any loan for that matter) is your MINIMUM payment. The sooner you pay them off, the less interest you pay, and the sooner you can have your life back.

(2)

Graduated Repayment Plan

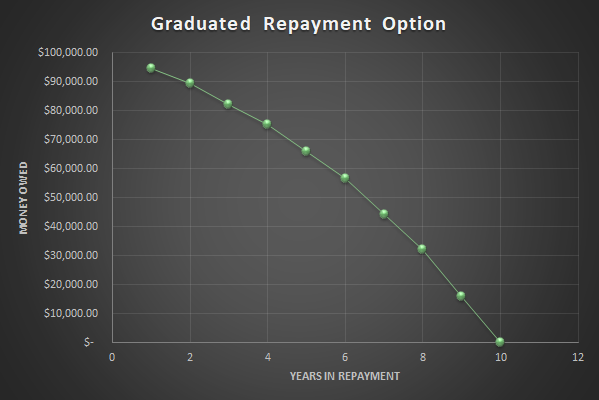

The next student loan repayment option is the Graduated Repayment Plan. With the Graduated Repayment Plan, your payments start out pretty small but then get bigger every two years. Typically this type of loan repayment is done over 10 years but it can be stretched out all the way to 30 years. Sometimes, this can be good because the smaller payments at the beginning of your loan can be nice. But, as time goes on and you start getting car payments, credit cards, mortgages, and other debt, the student loan payments that you would pay towards the end of your loan can be pretty big. For example, if you have $100,000 in student loans and do the 10-year graduated repayment plan, for the first two years your payments will be about $447/month. Not bad, right? But for the last two years your payments would be about $1,340/month. Ouch.

Here are some pros and cons of the Standard Repayment Plan as well as a graph of what it looks like in the 10 year graduated repayment plan.

Pros:

- You will pay less interest than most of the other plans over time (except for the standard repayment plan) if you go with the 10-year option.

- Your payments are pretty affordable at the beginning of your loan.

- Even when your payments are small at the beginning of your loan, they will always be at least the amount of accrued interest on the loan (so it is always going down in value).

Cons:

- The payments can be pretty massive toward the end of your loan.

- You will pay more interest than the standard repayment plan over time.

For the second time, remember, you can (AND SHOULD) pay extra on your student loans to pay them off sooner. Your payment on your student loans (or any loan for that matter) is your MINIMUM payment. The sooner you pay them off, the less interest you pay, and the sooner you can have your life back.

(3)

Extended Repayment Plan

The third student loan repayment option is the Extended Repayment Plan. The Extended Repayment Plan is almost the same as the first two plans that you read about. The only difference is that the Extended Repayment Plan is over 25 years rather than the typical 10 years for the standard repayment plan or the graduated repayment plan. In order to qualify for this repayment option, you must have a minimum of $30,000 in federal student loans.

With the Extended Repayment Plan, you can choose to pay it back as a standard repayment option. Remember, this is where your payments stay the same over the life of the loan and you will pay less interest over time. Or you can choose to pay it back as a graduated repayment plan. Also remember that this is where your payments start out small and increase every two years until you pay the student loan off.

It is important to know that with the Extended Repayment Plan (either with the standard repayment option or the graduated repayment option) you will pay a lot more interest over the life of the loan because the payments are dragged out for 25 years rather than just paying them off in 10 years like the first two options.

Here are some pros and cons of the Extended Repayment Plan as well as a graph of what it looks like in the 25 year standard and graduated repayment plan.

Pros:

- With the extended plan your payments will be smaller than the standard or graduated plans. If you have a ton of student loan debt, this can help ease your budget a little.

Cons:

- You will pay a lot more interest over time.

- You will have the payment for 25 years. Think about that. That is most of your working life. Do you really want to have your student loans hanging around that long?

For the third time, remember, you can (AND SHOULD) pay extra on your student loans to pay them off sooner. Your payment on your student loans (or any loan for that matter) is your MINIMUM payment. The sooner you pay them off, the less interest you pay, and the sooner you can have your life back. This is especially true with a loan that is supposed to drag out for 25 years.

(4)

Revised Pay As You Earn (REPAYE) Plan

The fourth student loan repayment option is the REPAYE. The REPAYE plan starts to get a little trickier. If you choose this plan the payments will probably change every year (sort of like the graduated repayment plan). One of the differences is that the payments can get bigger or smaller depending on what your income does. So for example, if you are just out of college and not making much money, you may have a small payment (or even no payment at all). But after a couple years of working you get a huge raise and a promotion and your pay goes up, so will your student loan payment. But in the future, if you take a different job for less money, your payment will go down. This repayment plan also takes into account your spouse’s income (if you have a spouse) to figure out your payment.

The REPAYE plan will never give you a payment that is more than 10% of your discretionary income. For this student loan repayment plan, discretionary income is defined as your income minus 150% of the poverty line guidelines for your state. You can find the poverty line here.

[Your Income – (150% * poverty line)] * 10% = Your Annual Payment

Your Annual Payment / 12 = Your Monthly Payment

You can do it! You went to college!

The REPAYE plan is based on a few things:

- The poverty line in your state (all states use the federal poverty line except for Alaska and Hawaii).

- The number of people in your family.

- Your income.

A lot of people flock to this repayment plan (and the other ones that I’m getting ready to discuss) because these plans have lower payments. However, the downside of this is that because your payments are so much lower at the beginning, often when you make your payments the payment amount doesn’t even cover the interest! That means that the balance is actually going up. Please don’t let the balance go up. It’s a horrible cycle that will get worse and compound.

The REPAYE plan is for federal student loans taken out before 2011 (we’ll get into this in the next section.

For undergraduate loans, through the REPAYE plan, the loans are supposed to be forgiven after 20 years even if you have a remaining balance. For graduate loans they are supposed to be forgiven after 25 years. Please don’t stop reading right now though because you have supposedly found the loan repayment plan that gives you forgiveness. The federal government can change the plans of any government plan at any time.

So in the next 20-25 years, the federal government could change or even eliminate the program. And also, the federal student loan forgiveness programs have a horrible track record so far. Only about 1% of student loan borrowers who have applied for forgiveness have actually been forgiven (discussed at the beginning of this article).

Here are some pros and cons of the Revised Pay As You Earn (REPAYE) plan as well as a graph of what it looks like in the 20 and 25 year repayment plan for an average family (assuming that the federal government actually does forgive the loans).

Pros:

- A much lower payment than most of the other repayment plans.

- Payments can be very small (or even $0/month at the beginning of repayment)

- The federal government will forgive the remaining balance after 20 years for undergraduate loans and 25 years for graduate loans (hopefully).

Cons:

- You may not even pay off the accrued interest at the beginning of the loan.

- You have to rely on the federal government (which has a long history of changing government programs) to pay off the remaining balance of your student loans.

For the fourth time, remember, you can (AND SHOULD) pay extra on your student loans to pay them off sooner. Your payment on your student loans (or any loan for that matter) is your MINIMUM payment. The sooner you pay them off, the less interest you pay, and the sooner you can have your life back. This is especially true with a loan that is supposed to drag out for 25 years.

(5)

Pay As You Earn (PAYE) Plan

The next student loan repayment option is the PAYE. The PAYE plan is almost the exact same as the REPAYE (that was discussed in the previous option). The only negligible difference is that with the PAYE plan, your payment can never be more than it would on the 10 year standard payment would be.

For example, if you decide to use the PAYE plan to pay back your student loans and you aren’t making much money and your payment might be only $50/month. But if you were to choose the standard repayment program instead your payment would be $1,000/month. That means that if you are using the PAYE plan and you get a big promotion and start making millions of dollars per year, your payments will still never be more than $1,000/month. Even though 10% of your discretionary income is probably way more than $1,000/month.

For everything else you need to know about the PAYE plan, just look at the REPAYE plan (#4 in this list).

Here are some pros and cons of the Pay As You Earn (PAYE) plan as well as a graph of what it looks like in the 20 and 25 year repayment plan for an average family (assuming that the federal government actually does forgive the loans).

Pros:

- A much lower payment than most of the other repayment plans.

- Payments can be very small (or even $0/month at the beginning of repayment)

- The federal government will forgive the remaining balance after 20 years for undergraduate loans and 25 years for graduate loans (hopefully).

Cons:

- You may not even pay off the accrued interest at the beginning of the loan.

- You have to rely on the federal government (which has a long history of changing government programs) to pay off the remaining balance of your student loans.

I know I sound like a broken record, but for the fifth time, remember, you can (AND SHOULD) pay extra on your student loans to pay them off sooner. Your payment on your student loans (or any loan for that matter) is your MINIMUM payment. The sooner you pay them off, the less interest you pay, and the sooner you can have your life back. This is especially true with a loan that is supposed to drag out for 25 years.

(6)

Income Based Repayment (IBR) Plan

The sixth student loan repayment option is the IBR. The Income Based Repayment Plan works similarly to the PAYE and REPAYE plans. There is one main difference that has to do with the size of the payment. If you took any federal student loans out BEFORE July 1, 2014 your payment will be 15% of your discretionary income. If you did not take out any federal student loans until AFTER July 1, 2014 your payment will be 10% of your discretionary income.

Remember, as discussed before, for this student loan repayment plan, discretionary income is defined as your income minus 150% of the poverty line guidelines for your state. You can find the poverty line here.

[Your Income – (150% * poverty line)] * 10% = Your Annual Payment

Your Annual Payment / 12 = Your Monthly Payment

You can do it! You went to college!

Everything else is pretty much the same as the PAYE plan.

Here are some pros and cons of the Income Based Repayment (IBR) plan as well as a graph of what it looks like in the 20 and 25 year repayment plan for an average family (assuming that the federal government actually does forgive the loans).

Pros:

- A much lower payment than most of the other repayment plans.

- Payments can be very small (or even $0/month at the beginning of repayment)

- The federal government will forgive the remaining balance after 20 years for undergraduate loans and 25 years for graduate loans (hopefully).

Cons:

- You may not even pay off the accrued interest at the beginning of the loan.

- You have to rely on the federal government (which has a long history of changing government programs) to pay off the remaining balance of your student loans.

I hope you are starting to notice how serious I am when I say for the sixth time, remember, you can (AND SHOULD) pay extra on your student loans to pay them off sooner. Your payment on your student loans (or any loan for that matter) is your MINIMUM payment. The sooner you pay them off, the less interest you pay, and the sooner you can have your life back. This is especially true with a loan that is supposed to drag out for 25 years.

(7)

Income-Contingent Repayment (ICR) Plan

The seventh student loan repayment option is the ICR. Pretty much everything is the same with the Income-Contingent Repayment plan as the PAYE, REPAYE, and IBR plans. The ICR plan is a lot like the PAYE, REPAYE, and IBR plans except for the big difference once again has to do with the size of your payments.

With the ICR plan your payments will be the LESSER of

- 20 % of your discretionary income that is calculated just like the REPAYE, PAYE, and IBR plans. Here is the formula

[Your Income – (150% * poverty line)] * 10% = Your Annual Payment

Your Annual Payment / 12 = Your Monthly Payment

You can do it! You went to college!

- Or your payment amount on a Standard Repayment plan (just like in #1) that is for 12 years instead of 10 (like the Standard Repayment plan).

For most people, that will mean that their payments will be calculated based on the first option.

As I stated before, pretty much everything else is the same as the PAYE, REPAYE, and IBR plans.

Here are some pros and cons of the Income-Contingent Repayment (ICR) plan as well as a graph of what it looks like in the 20 and 25 year repayment plan for an average family (assuming that the federal government actually does forgive the loans).

Pros:

- A much lower payment than most of the other repayment plans.

- Payments can be very small (or even $0/month at the beginning of repayment)

- The federal government will forgive the remaining balance after 20 years for undergraduate loans and 25 years for graduate loans (hopefully).

Cons:

- You may not even pay off the accrued interest at the beginning of the loan.

- You have to rely on the federal government (which has a long history of changing government programs) to pay off the remaining balance of your student loans.

FOR THE SEVENTH TIME, remember, you can (AND SHOULD) pay extra on your student loans to pay them off sooner. Your payment on your student loans (or any loan for that matter) is your MINIMUM payment. The sooner you pay them off, the less interest you pay, and the sooner you can have your life back. This is especially true with a loan that is supposed to drag out for 25 years.

(8)

Income Sensitive Repayment (ISR) Plan

This type of student loan repayment option will not affect many people. Income Sensitive Repayment (ISR) plans are only used for FFEL loans. If you don’t know what an FFEL loan is, don’t worry about it. Most borrowers have Direct Loans, not FFEL loans.

The FFEL loan program stopped in July 2010 so if you only have loans that have been taken out after then, you don’t need to worry about this plan.

Basically, FFEL loans can be paid back with the ISR plan if you choose.

With the ISR plan the payments are made over a 15 year period and adjust to your income as needed. The loans will be paid off at the end of the 15 year period and there is no student loan forgiveness on FFEL loans as you might get with the PAYE, REPAYE, IBR, and ICR plans.

Here are some pros and cons of the Income Sensitive Repayment (ISR) plan. There is no graph for this loan repayment type that I could make because the payments can vary wildly. Just remember that the loan will be paid off in 15 years.

Pros:

- Loan will be paid off in 15 years.

- FFEL loans are usually smaller because the cost of college was less prior to 2010.

Cons:

- They are not eligible for any type of forgiveness.

- If you have FFEL loans and want to use one of the other repayment plans (#1-7), you have to consolidate your FFEL loans into Direct Loans first.

- The payments can vary wildly.

Ok, last time, remember, you can (AND SHOULD) pay extra on your student loans to pay them off sooner. Your payment on your student loans (or any loan for that matter) is your MINIMUM payment. The sooner you pay them off, the less interest you pay, and the sooner you can have your life back. This is especially true with a loan that is supposed to drag out for 25 years.

To Make a Long Story Short…

To find out what your payment would be based on your current situation go to the Federal Student Loan Payment Simulator website and put in all of your information.

If you want to pay off your student loans the fastest and pay the least interest: look into the Standard Repayment plan (#1).

If you want to pay your student loans off the fastest but your income might be a little low at first: look into the Graduated Repayment plan (#2).

If you want the same payment over time but have a truck-load of student loans: look into the Extended Standard Repayment plan (#3).

If you want to make smaller payments that will get bigger over time because your income might be a little low and you have a truck load of student loans: look into the Extended Graduated Repayment plan (#3).

If you want (likely) the smallest payment that will change over time and want to depend on the government to pay off your student loans in 20 or 25 years: look into the PAYE, REPAYE, IBR, or ICR plans (#4, 5, 6, and 7).

If you have FFEL student loans: look into the ISR plan (#8).

That is a LOT of information. I hope that I have helped and you have been able to exercise your Money Muscle.

If you want to learn more about student loans, how they work, and how you can tell them to GTFO, check out my other articles here.

I really enjoy writing these articles for all of you. I’ll be back here later to give you guys another piece of information and help so that you can continue to grow your Money Muscle and become more fiscally fit. Until next time!

0 Comments